Overview & Concept

TDS has to be deducted not only for salary payments but also for other payments including rentals, interest, fees, commissions, etc. All these non-salary TDS deductions are covered under a comprehensive Form 26Q. The Income Tax Act also defines threshold beyond which TDS has to be deducted and also the rates of TDS applicable in each of these cases. While making payments to the payee, the payer has to deduct TDS based on pre-set thresholds and at the extant rates. All payments other than salary are covered under Form 26Q and the returns for the same have to be filed on a quarterly basis. The total amount paid to concerned persons along with their respective PAN numbers and the amount so deducted has to be disclosed in detail as part of Form 26Q.

On What Transaction TDS is Applicable ?

Section 26Q covers the following transactions on which TDS is applicale :

- Section 193 – Interest on securities

- Section 194 – Dividend

- Section 194A – Other Interest

- Section 194B – Winnings from lotteries and crossword puzzles

- Section 194BB – Winnings from horse race

- Section 194C – Payment to contractors and subcontractors

- Section 194D – Insurance commission

- Section 194EE – Payment in respect of deposit under NSS

- Section 194F – Payments on account of repurchase of Units by Mutual Funds

- Section 194G – Commission, prize on sale of lottery tickets

- Section 194H – Commission or Brokerage of any form

- Section 194I(a & b) – Rent

- Section 194J – Fees for Professional or Technical Services

- Section 194LA – Compensation on acquisition of certain immovable property

- Section 194LBA – Income from units of a business trust

- Section 194DA – Payment in respect of life insurance policy

- Section 194LBB – Income in respect of units of investment fund

- Section 194IA – Payment on transfer of non-agricultural immovable property

- Section 194LBC – Income in respect of investment in securitization trust

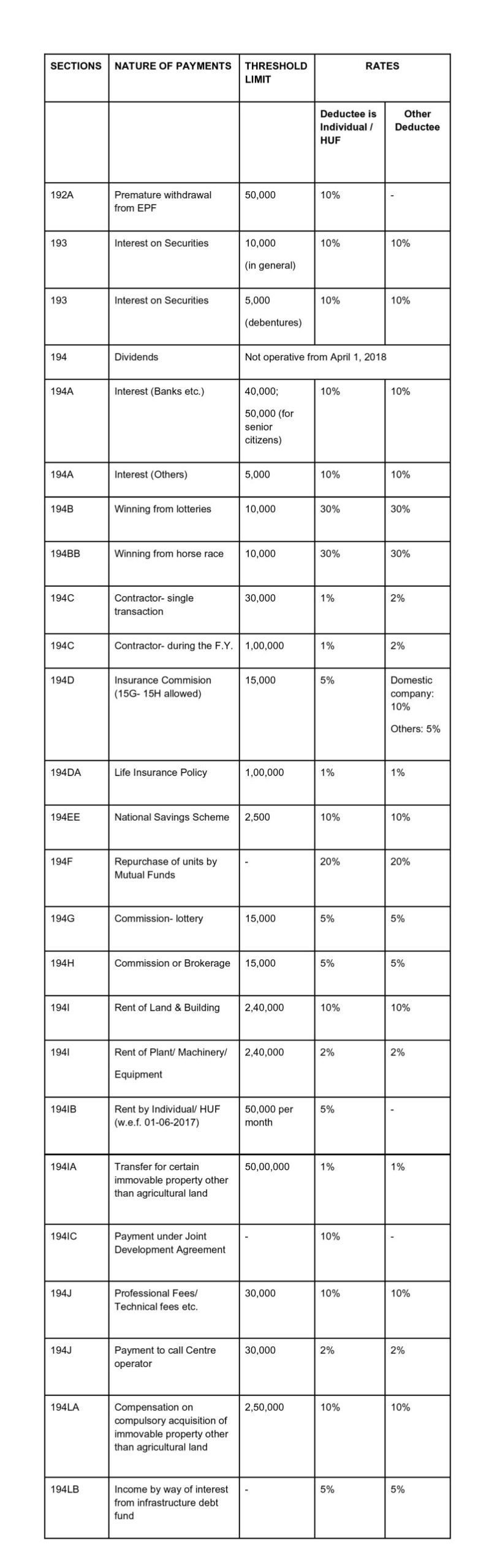

What are the TDS rate Applicable ?

Following is the Rate Chart on which TDS is applicable:

What are the Due Dates for TDS Return Filings ?

The Following the Due Dates for Fining 24Q NON Salary Return :

QUARTER | QUARTER PERIOD | DUE DATE |

1st Quarter | 1st April to 30th June | 31st July |

2nd Quarter | 1st July to 30th September | 31st October |

3rd Quarter | 1st October to 31st December | 31st January |

4th Quarter | 1st January to 31st March | 31st May |

What are the consequences for NON Filing of TDS Return ?

- It is incumbent to file the Form 26Q on time. There are penalties for non-deduction of TDS, non-payment into the government account and other delays.

- If TDS is not deducted, where due, penal interest of 1% per month will be charged from due date to actual deduction date.

- If TDS deducted is not deposited, penal interest at 1.5% per month will be charged from date of deduction to actual payment.

- Under Section 234E, late filing fee of Rs. 200 per day is to be paid until the return is filed. This amount applies to each day until the total fine becomes equal to the TDS.

- In addition, the tax department may also charge penalty of minimum Rs10,000 and maximum Rs1,00,000 under Section 271H. This penalty is waived if returns are filed within 1 year of the due date and the TDS and other fines are paid.

- Finally, as a measure of safety, ensure that you verify all the PAN numbers, challan numbers and also match the same with details available in the OLTAS and the NSDL websites. This can make your job easier.